Natural Disasters, Employment Opportunities, Vendor Services; Weekly Jobless Claims

California is currently going through a heat wave (Sacramento set a temperature record on Tuesday at 116°), taxing the state's power grid as energy demand breaks records and power officials request homeowners to turn down their air conditioning. A break in the heat could come due to Hurricane Kay bearing down on the state, which would mean California may be trading the heat for flooding. Did you know that 66 percent of Americans don’t feel fully prepared for potential natural disasters, with many lacking key emergency preparedness items such as generators, emergency evacuation kits, and radios? You're more likely aware that the hot housing market continues to cool. Home sales are falling in response to rising interest rates and there’s still a mismatch of supply and demand. Fannie Mae reported that high home prices and mortgage rates weighed on housing sentiment in its August Home Purchase Sentiment Index (HPSI), which posted the sixth consecutive monthly decline. Ivy Zelman’s forecast model predicts that in 2023 U.S. home prices will fall 4 percent before another 5 percent drop in 2024 due to rising inventory levels and falling demand. Though not everyone agrees with Zelman’s outlook: Zillow predicts that U.S. home prices will rise another 2.4 percent next year while Goldman Sachs predicts that U.S. home prices will rise 1.8 percent in 2023 and 3.5 percent in 2024, as does CoreLogic, Fannie Mae, and Freddie Mac. (Today’s podcast is available here and includes an interview with Tom Booker on the reduction of repurchase risk for mortgage lenders. This week’s podcasts are sponsored by Candor, home of the One Touch Underwrite, supporting lenders from Point of Sale to Post Close QC. Reduce repurchase risk, increase underwriter productivity by 400 percent, and decrease turn-times by 10 days.)

Vendor Services

There are a number of new and interesting ideas for MBS futures and derivatives that will soon be coming to market. However, another new idea percolating that serves an immediate need is an exchange-traded TBA option that settles in cash. The patented idea has been proposed by Mortgage Option Concepts LLC, a venture founded by industry veteran Bill Berliner. The contracts would not have any securities delivered against exercises and funds would simply be transferred between accounts, eliminating the delivery process and saving on transaction costs. Such a market would be liquid, transparent, and allow mortgage market participants of all sizes to utilize options effectively. They’re working diligently to generate interest in the concept among traders, mortgage hedgers, and liquidity providers. If you’re a market participant and would like more information, email for a package that describes the proposed market and how to proceed.

It’s budget season! Time to evaluate your technology gaps and identify solutions that address your business goals for each product and consumer segment. To guide you through the decision process, download Manage Your Tech Stack to Align With Your Changing Business Needs, which also highlights various benefits of calibrating your tech stack to gain budgetary approval. The paper provides best practices for gaining adoption of new tech with a three-phase implementation plan, which can also be used to relaunch any technology platform that is not being fully utilized. After your tech analysis, if you’re in the market for a consumer-focused solution to complement your existing tech stack for lead gen, lead nurturing, conversion and retention that your company can privately brand, watch the online FinLocker demo or schedule a 1:1 meeting to preview FinLocker’s latest features.

Does your subservicer oversight review simply meet compliance requirements, or does it provide you with valuable insights to improve your operation and allow you to see how your subservicer is complying with new regulations and agency requirements? Richey May’s review enables you to play a more active role in the servicing of your loans and take proactive action to drive true value for your business. And if you’re not sure whether you should continue to retain servicing in this market, Richey May can work with you to develop the optimal released/retained strategy. By leveraging the team of mortgage industry experts at Richey May, you will gain valuable insights that help your entire operation. Learn more about Richey May’s subservicer oversight reviews and servicing strategy deep dives.

Trivia time! How well do you really know Optimal Blue? Sure, you’re probably familiar with their industry-leading product, pricing and eligibility (PPE) engine, which is used for 40 percent of locks nationwide. And you surely know about their renowned trading and hedging teams, which process over $3.5 trillion in transactions annually. But believe it or not, there’s something else that sets Optimal Blue apart: their industry experts. This renowned team works directly with Optimal Blue clients to support not only their current needs, but also their long-term success. You may wonder why Optimal Blue goes so far above and beyond to offer each client personalized service. The answer is simple. When their clients succeed, they succeed, and the larger industry does too. Whether you’re an existing Optimal Blue client, or you’re looking for a strategic partner to support your pricing and hedging strategies, contact us today.

“At Cenlar, we are always striving to improve the homeowner experience and deliver service that outpaces industry benchmarks. The results of our efforts are clear, with the kind of progress that is measurable. Our call center is consistently outpacing industry benchmarks. Our performance reflects both our investments in people and technology, and the strengthening of our commitment to “think like a homeowner.” We strive to anticipate homeowner needs and answer common questions through proactive communications, like our chat bots and web site. While it is important to us that we are among the best in our industry, it’s of even greater importance that we are always improving the service we deliver to our clients and their homeowners. Let’s discuss how Cenlar can meet the mortgage servicing needs of your organization. Call 1-888-SUBSERV (782-7378) or visit us.”

Are you ready to DU?! Did you know you can run DU/DO and follow your findings with ClearEdge Lending’s Flex Connect? It’s not just for full or express doc, but it also works for bank statement loans, too. Follow DO/DU including no reserves on bank statement loans, no VOR’s, no payment shock, 40 year I/O, and 100% gift allowed. Flex Connect has been described as “Non-QM so easy, it feels like agency” and it works on all occupancy types, all transaction types, up to 80% LTV, $2.5 MM max loan amount, and FICOs as low as 640. Work with ClearEdge to access experienced professionals who provide in depth bank statement review within 24 hours, fast submissions and locks, set up and disclosures in less than a day, collaboration to resolve conditions, one closer for docs and funding, and so much more! Find out why originators are raving about ClearEdge Lending’s service and easy-to-close lending solutions, contact us today or call us (866) 690-2474.

Have you left money on the table due to purchase advice errors? Join MCT for a webinar today at 10am PT discussing the benefits of MCTlive! integrations with Fannie Mae technology. MCT recently became the first platform integrated with the Fannie Mae Connect Whole Loan Purchase Advice Seller API, allowing clients to pull purchase advice data to MCTlive! directly out of Fannie Mae. This API connection allows MCT Mark-to-Market and Hedge Accounting Reports to be updated with Fannie Mae purchase data instantly, instead of waiting to run reports through a LOS. Clients of MCT can also pull live note pricing and Servicing Marketplace executions through an API, allowing for delivery of multiple commitments with one click through Rapid Commit within MCTlive!, MCT’s award-winning best execution & loan pipeline management software. Register for today’s webinar and contact MCT to start the process of automating purchase advice for whole loan buyers or sellers.

Rocket Pro TPO’s new products and new Non-Delegated Correspondent lending solutions are waiting for you! We’re getting ready to add more to our product mix this Fall – designed to grow, nurture, and retain clients! It starts with our highly anticipated new Home Equity Loan. Get all the details about upcoming products at Austin Niemiec’s live webinar on Thursday, September 8. Click this link to sign up. In addition to great products, partners are now experiencing our new Non-Delegated Correspondent fulfillment options. Sign up today to join our partners who are already leveraging Rocket technology for all their disclosure needs including closing documents! Contact Rocket Pro TPO today to learn more.

Updates From Fannie, Freddie, and Ginnie

Freddie Mac reminded users that with the new loan program identifiers, lenders will no longer require the manual workaround to include improvement costs in the purchase price data field for CHOICERenovation, CHOICEReno eXPress and GreenCHOICE. On September 26, 2022: A new loan program identifier will be implemented in LPA and Loan Selling Advisor for mortgages secured by income-based resale restricted properties. A new loan program identifier will be available in Loan Quality Advisor and Loan Selling Advisor for CHOICERenovation mortgages with recourse. As a reminder, the community land trust mortgage loan program identifier has been available since March 28.

Freddie Mac provides information to homeowners about discriminatory restrictive covenants that may be attached to their properties. In the Frequently Asked Questions shared, homeowners can learn about restrictions on their real estate, their meaning, and what property owners may be able to do about them. Look for additional information on discriminatory restrictive covenants coming soon. Visit our Single-Family EQH web page to learn more about Freddie Mac’s work with equitable housing.

Freddie Mac Single-Family Seller/Servicer Guide Bulletin 2022-16, announced, information on properties with age-based resale restrictions, revised automated collateral evaluation (ACE) eligibility, revised Loan Collateral Advisor® eligibility for representation and warranty relief for value, defining partial income representation and warranty relief through our Loan Product Advisor® asset and income modeler (AIM) income offerings, Fidelity insurance requirements, an update to the requirements for fidelity insurance coverage for subservicers effective August 10, 2022. Additionally, Bulletin 2022-16 includes additional Guide updates on eMortgages and other topics that may be important to your business.

Freddie Mac’s Single-Family business today announced that its Credit Risk Transfer (CRT) program reported Second Quarter 2022 CRT issuance of approximately $6.5 billion, protecting approximately $151 billion in unpaid principal balance (UPB) of single-family mortgages. The total was a record for a second quarter. Additionally, record first half 2022 issuances totaled nearly $15 billion, protecting $358 billion UPB of single-family mortgages. The issuances included our flagship STACR® (Structured Agency Credit Risk), and ACIS® (Agency Credit Insurance Structure) transactions, as well as other risk sharing transactions.

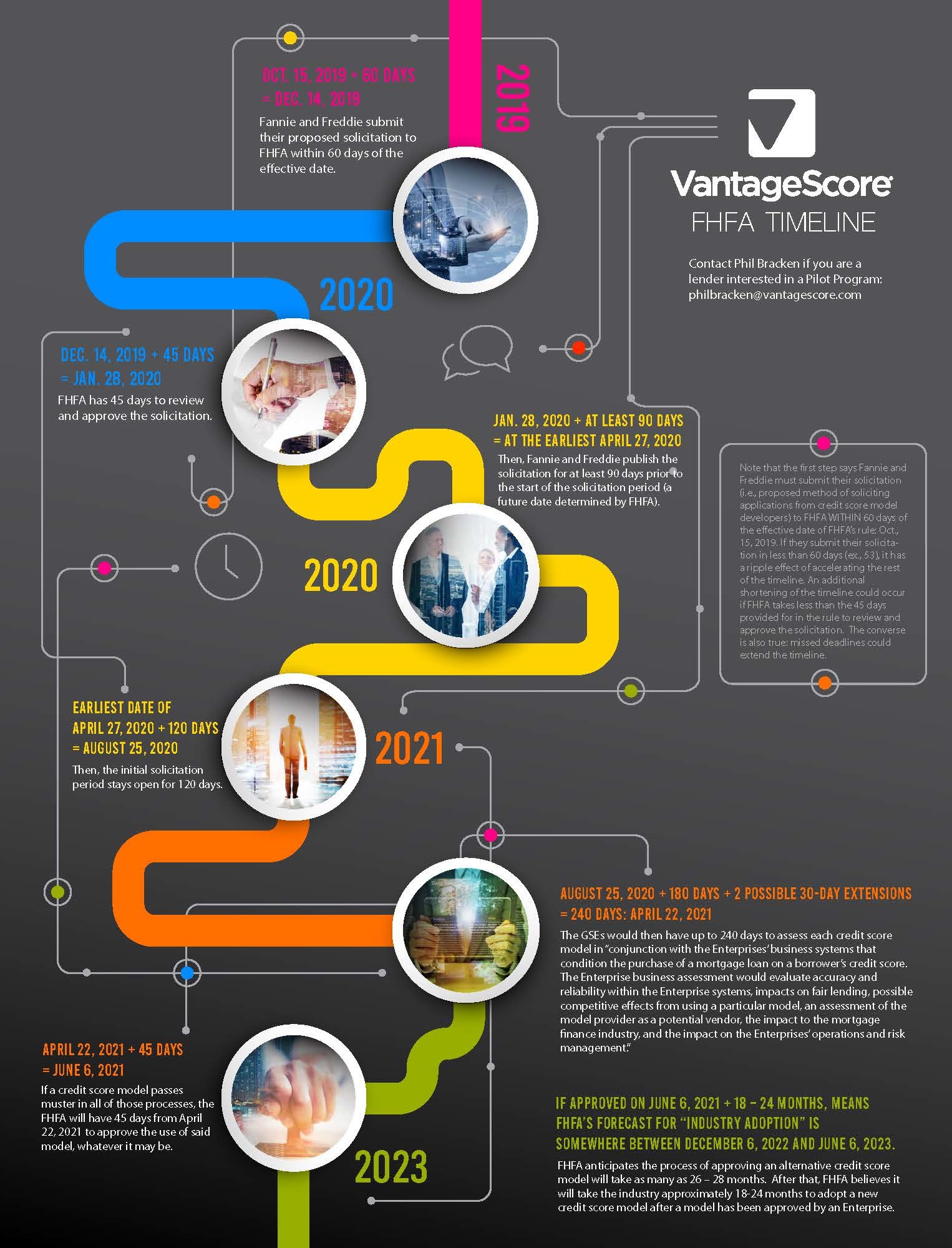

During a March 2022 FHFA listening session, four options were outlined for incorporating another credit scoring into the GSEs’ underwriting process: Single Score: The GSEs require delivery of a single score either FICO 9 or VantageScore 3.0, if available, on every loan; Require Both: The GSEs require delivery of both scores, if available, on every loan;

Lender Choice: The GSEs would allow lenders to deliver loans with either score, when available, with certain constraints such as using one score or the other for a defined period of time; and Waterfall: The GSEs would allow delivery of multiple scores through a waterfall approach that would establish a primary credit score and secondary credit score.

While it is our understanding that the GSEs are working to implement VantageScore into the underwriting process, it is unclear which, if any, if these options were selected. After the listening session, there was a push for Option 3) Lender Choice. In our view, Lender Choice would be aligned with the administration’s goals of increasing access to affordable housing and affordable credit, but we will have to wait for the FHFA’s announcement to know the outcome.

Marcus Lam from Flagstar points out that, “For Agency loans, credit card reward points as acceptable funds for use towards closing costs, down payment and financial reserves, provided the reward points are converted to cash prior to the closing of the loan. The following requirements apply: (1) If the credit card reward points are converted to cash and deposited into the borrower’s depository account (for example, checking or savings), no additional documentation is required unless the deposit is considered a large deposit. (2) If the credit card reward points are converted to cash, but not deposited into a borrower’s depository account, provide evidence the reward points were available to the borrower prior to the conversion, including verification of the cash value (for example, credit card reward statement prior to conversion); and converted to cash prior to the closing of the loan. Asset type must be indicated as “Other”.

Compass Point Research & Trading’s Ed Groshans summed up current credit developments well. “We received inquiries asking when FHFA or the GSEs will make announcement on the VAP process for VantageScore. Our work indicated that then FHFA Director Sandra Thompson would not address the issue until after being confirmed by the Senate. Thompson was confirmed as FHFA Director on May 25, 2022. We followed up on the issue with SitusAMC Head of Industry Relations Tim Rood. It is our understanding that the GSEs have completed the validation phase for VantageScore. The next steps involve working with originators to implement VantageScore into the underwriting systems (FNMA’s Desktop Underwriter, FMCC’s Loan Prospector). The rollout is expected to occur in 1Q23. This is in line with the estimate published by VantageScore in 2019 (Figure 1). Prior to going live, we anticipate that FHFA will issue a press release stating that the validation and approval of VantageScore for use by FNMA and FMCC. We expect the Federal Housing Administration (FHA) will also include VantageScore into its underwriting system, but this will occur after the GSEs complete their system rollout.

{kind=link}

Fannie Mae introduced a proposed methodology for single-family social disclosure. It aims to provide investors with insights into socially oriented lending in a creative and unique way that is designed to help preserve the confidentiality of the mortgage consumer's personal information.

With this Perspectives article, we This methodology was designed with investors' needs in mind. We encourage feedback and are excited to engage with market stakeholders in refining the methodology's design. More information is available in Fannie Mae’s Perspective Article: Designing for Impact – A Proposed Methodology for Single-Family Social Disclosure.

The newest legal documents available from Fannie Mae are posted here.

Fannie Mae’s Selling Notice - Quality Control Calibrations introduces Quality Control Calibrations, an expanded and formalized initiative to engage with a larger segment of our lenders in the calibration of their QC results. In QC, calibration is the process of comparing a lender’s own internal QC results to a known measurement, or standard, to confirm the accuracy of the lender’s results.

Fannie Mae posted information on its shared responsibility to protect data, both its own proprietary business data and non-public personal information such as mortgage borrower data. Fannie Mae is entrusted with a significant amount of industry and borrower data and has a rigorous information security program to help protect it, plus requirements for our business partners to follow in the event of a data breach (including a ransomware attack).

Ginnie Mae (GNMA-private) recently published its revised Single-Family Applicant and Issuer Financial Eligibility Requirements. The release follows its July 2021 Request for Input (RFI) on Eligibility Requirements for Single Family MBS Issuers. The revisions increased servicers net worth capital and liquidity requirements and added a new risk-based capital (RBC) requirement. The changes could pose a challenge for smaller servicers and entities that are not well capitalized. It could reduce access to affordable single mortgage credit for underserved communities. On August 17, 2022, GNMA introduced a risk-based capital requirement for servicers. On December 31, 2023, servicers will have to meet an RBC requirement of 6 percent, below the 10% level that was proposed. The RBC capital requirement and calculation is based on the banking capital requirements that were implemented in 2018. On its face, 6 percent does not appear to be an onerous capital requirement; however, the calculation will negatively affect institutions that have mortgage servicing rights (MSR) that materially exceed their capital levels as well as other assets that have a risk weight of 0% or 20%, such as cash or loans, that represent a small proportion of assets. First, MSRs in excess of capital are deducted from capital (ANW), as proposed (Figure 1). Second, the MSR risk weight was set at 250% for all MSRs at or below the capital base, as proposed. No risk weight is assigned to MSRs that are above the capital base as these are deducted from it.

Capital Markets

Expectations that the Federal Reserve will continue robust interest-rate increases have pushed the yield on the 30-year Treasury to the highest point since 2014. Cleveland Fed president Mester offered a very hawkish speech yesterday, reiterating that taming inflation comes first and everything follows from that. "Price stability is necessary for ensuring that the U.S. can sustain healthy labor market conditions over the medium and longer run," she said. “Before I conclude that inflation has peaked, I will need to see several months of declines in the month-over-month readings. It will be necessary to move the nominal fed funds rate up to somewhat above 4 percent by early next year and hold it there; I do not anticipate the Fed cutting the fed funds rate target next year"

She did provide some thoughts on balance sheet reduction: "The reduction in our balance sheet is being done primarily by adjusting how much we reinvest of the principal payments we receive on our assets. Without asset sales, the process could take three years or so. I would favor the FOMC’s considering selling some of our agency mortgage-backed securities at some point during balance-sheet reduction in order to speed the return of our portfolio’s composition to being primarily Treasury securities. One potential way to implement sales would be to sell agency securities up to the cap in any month in which principal payments were less than the cap. This is similar to our treatment of Treasuries. Another way to implement sales would be to set a monthly floor on reductions, which would be met first by principal payments received and then by sales."

Traders continue to assess market data before the FOMC meeting at the end of the month to see how far the central bank will go in its battle against inflation. The thinking is that the more positive the economic figures, the less the Fed will have to worry its aggressive hiking cycle will trigger a downturn. Today’s potential highlight was the latest ECB decision, which yielded a 75-basis point rate hike, as well as ECB head Lagarde’s press conference shortly after. Domestically, Fed Chair Powell is also scheduled to speak alongside Chicago Fed President Evans. Weekly jobless claims were released, registering at 222k. Later this morning brings Freddie Mac’s Primary Mortgage Market Survey and July Consumer Credit. Today’s MBS purchase operation, the last of the week with only two operations remaining afterwards, sees the Desk in GNII 4 percent through 5 percent for up to $386 million. We begin the day with Agency MBS prices better by a couple of ticks and the 10-year yielding 3.23 after closing yesterday at 3.22 percent.

Employment

Planet Home Lending is happy to announce that proven team-builder Regional VP Kathryn Edelen (301-502-2493), who is currently adding to their national footprint in the East, has been joined by newly hired Regional VP Lynette Hale-Lee (818-321-1260) in the West. Hale-Lee, a long-time mortgage professional who brings extensive experience to her new role,says Planet is “exceptionally and unusually well-positioned to move through challenging markets now and over the next few years.” What sets Planet apart? Data-driven marketing. Award-winning servicing. Leadership like CEO and President Mike Dubeck who knows both Wall Street and Main Street. Add to that an enviable tech stack and a wide array of niche products, and it’s no wonder Planet is growing, even during this period of market shifts and rising interest rates. Reach out to Planet Home Lending’s Kathryn Edelen or Lynette Hale-Lee, call VP of Talent Acquisition Peter Briggs (435-709-6287), or visit here.

Guardian Mortgage is expanding its loan origination staff in all key markets. At Guardian Mortgage, they're proud of customer loyalty and retention! Guardian focuses on retaining most loan servicing and maintaining the quality customer relationships their originators have formed in the 43 states where they lend. Their Loan Originators have helped generations of members of the same family obtain home loans. Jen Guidry, one of Guardian's top loan originators, shares the following insight about her experience moving to Guardian. "My biggest fears in moving to another company were the stress and problems that come with transitioning a never-ending pipeline to a new place. The onboarding team made the transition process at Guardian Mortgage the smoothest I have experienced in over 25 years. Top-notch help, and it has been the best move that I've made in my career." Explore the Guardian difference at today!